blog

2024-04-18

A Comprehensive Comparison of Power BI and Excel | EduPristine

A Comprehensive Comparison of Power BI and Excel Hey there, welcome back again! In today's data-driven world, the ability to Read More

2024-04-15

CMA vs MBA: Choosing the Right Path for Your Career Growth

CMA Programa vs. MBA: Choosing the Right Path for Your Career Growth Hey there, so good to have you back Read More

2024-04-13

Corporate Governance: A Comprehensive Guide by EduPristine

Corporate Governance: A Comprehensive Guide Welcome to our exploration of Corporate Governance! In this blog, we will delve into the Read More

2024-04-12

A Guide to Mastering Payroll Management by EduPristine

Mastering Payroll Management: A Comprehensive Guide to Components, Compliance, and Accounting Entries Hey there, welcome back to our new blog. Read More

2024-04-11

Data Analytics for Management Accountants – EduPristine

Data Analytics for Management Accountants Why Data Analytics Matter for Management Accountants Hey there, so good to have you back Read More

2024-04-09

Investment Valuation: A Comprehensive Guide by EduPristine

Investment Valuation: A Comprehensive Guide Welcome to our comprehensive guide on investment valuation! In this blog, we'll break down the Read More

2024-04-08

Mastering MS Excel: Empowering Accountants for Success | EduPristine

Mastering MS Excel: Empowering Accountants for Success. Hey there, welcome back to our new blog. In the intricate world of Read More

2024-04-05

Different Payment Methods for Merger & Acquisition | EduPristine

Different Payment Methods for Merger & Acquisition In the ever-evolving landscape of business, Mergers and Acquisitions (M&A) stand as pivotal Read More

2024-04-04

Internal vs External Financial Reporting by EduPristine

Internal vs External Financial Reporting Financial reporting is a critical aspect of any organization's communication strategy, serving as a bridge Read More

2024-04-03

Difference Between Equity Funds and Mutual Funds by EduPristine

Understanding the Difference Between Equity and Mutual Funds Equity investment and mutual fund investment are both popular choices for long-term Read More

2024-04-02

Navigating the ACCA Career Landscape with EduPristine

Navigating the ACCA Career Landscape: Opportunities in India and Beyond Hey there, so good to have you back again! In Read More

2024-04-01

Chief Financial Officer (CFO): A Complete Guide | EduPristine

Chief Financial Officer (CFO): A Complete Guide In the dynamic domain of corporate governance, one figure stands out as the Read More

2024-03-31

All About Merger and Acquisition by EduPristine

Merger and Acquisition (M&A)? Its What, Why, and When What is M&A? When people hear that a company has taken Read More

2024-03-31

What is Income Tax? Part Two by EduPristine

What is Income Tax? Part Two Income tax stands as a pillar of India's economic framework, shaping financial dynamics and Read More

2024-03-30

Understanding the Basics of Direct Taxation with EduPristine

Understanding the Basics of Direct Taxation Hey there, so good to have you back again! In the realm of accounting, Read More

2024-03-30

The Crucial Role of Ethics in Management Accounting | EduPristine

The Crucial Role of Ethics in Management Accounting Hey there so good to have you back again! Have you ever Read More

2024-03-29

What is Income Tax? Part one by EduPristine

What is Income Tax? Part One Income tax serves as a cornerstone in India's financial landscape, wielding significant influence over Read More

2024-03-29

Financial Reporting vs. Financial Accounting by EduPristine

Financial Reporting vs. Financial Accounting: Understanding the Basics In the world of business and finance, two key terms often come Read More

2024-03-28

How Do Firms Manage Financial Risk | EduPristine

How Do Firms Manage Financial Risk? Managing financial risk is a crucial responsibility for firms in today's dynamic business landscape. Read More

2024-03-28

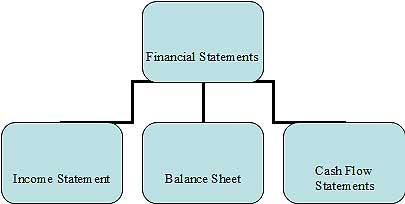

Financial Accounting and Types of Financial Statements | EduPristine

What is Financial Accounting? Exploring Types of Financial Statements Welcome to our exploration of Financial Accounting, a fundamental pillar of Read More

2024-03-27

Managerial Accounting- Its Meaning, Process and Types | EduPristine

What is Managerial Accounting? Its Meaning, Process and Types Hello and welcome to the world of managerial accounting—a practical and Read More

2024-03-27

A Guide on Project Finance by EduPristine

A Guide on Project Finance In the dynamic landscape of finance, where innovation and strategic thinking converge, one area that Read More

2024-03-26

Why do Finance Professionals use Power BI | EduPristine

Why do Finance Professionals use Power BI? Hey there, so good to have you back again! Have you ever found Read More

2024-03-25

Macroeconomics: Meaning, Process, and Indicators | EduPristine

Macroeconomics: Meaning, Process, and Indicators Welcome back, students! Today, we're delving into the world of macroeconomics. In this blog, we'll Read More

2024-03-23

Internal Audit- Meaning, Objectives, Types and Importance by EduPristine

Internal Audit- Meaning, Objectives, Types and Importance In the world of business, where things can get pretty complex, there's a Read More

2024-03-22

A Simple Guide on Quantitative Analysis- EduPristine

What is Quantitative Analysis? A Simple Guide In the ever-changing world of finance, where data holds immense power and decisions Read More

2024-03-22

Five Basic Principles of Accounting by EduPristine

What are the Five Basic Principles of Accounting? In the world of finance and business, accounting stands as the backbone, Read More

2024-03-21

Internal Controls: Meaning, Types, and Importance by EduPristine

Internal Controls: Meaning, Types, and Importance In the domain of business management, Internal Controls stand as the silent guardians ensuring Read More

2024-03-21

Basics of Accounting – Meaning and Basics Concepts | EduPristine

Basics of Accounting - Meaning and Basics Concepts Welcome to the world of Accounting 101 - where numbers tell a Read More

2024-03-20

The Different Business Functions by EduPristine

What are the Different Business Functions? In the dynamic landscape of commerce, businesses are intricate entities composed of various interconnected Read More

2024-03-20

The Different Types of Business Structures | EduPristine

What are Different Types of Business Structures? In the ever-evolving world of business, the key to sustained success goes beyond Read More

2024-03-01

The Vital Role of Cost Management for US-CMAs | EduPristine

The Vital Role of Cost Management for US-CMAs Hey there, so good to have you back again. Have you ever Read More

2024-02-16

Role of Ethics and Professionalism in the Investment Industry

Role of Ethics and Professionalism in the Investment Industry In the dynamic landscape of the investment industry, where fortunes are Read More

2024-02-13

The Risk Management Process: Essential Steps | EduPristine

The Risk Management Process: Essential Steps In the dynamic landscape of business and finance, uncertainties are inevitable. Every decision, venture, Read More

2024-02-07

ACCA vs CPA: Choosing the Right Path for Your Career | EduPristine

ACCA Certification vs. CPA Course: Choosing the Right Path for Your Career Embarking on a career in accounting opens a Read More

2024-02-05

Transforming Aspirations into Achievements: CPA Course Excellence

CPA Course Excellence: How EduPristine's Approach Transforms Aspirations into Achievements Embarking on the journey to become a US Certified Public Read More

2024-02-02

Comprehensive Guide to ACCA Certification with EduPristine

Unlocking Global Opportunities: A Comprehensive Guide to ACCA Training in India with EduPristine Welcome to your roadmap for global success Read More

2024-02-01

CPA Course Decoded: Achieve Success with EduPristine Training

CPA Course Decoded: Achieve Success with EduPristine's Expert-Led Training Embarking on the journey to become a US Certified Public Accountant Read More

2024-01-31

US CMA Course: A Step-by-Step Preparation Guide by EduPristine

Master the US CMA Course: A Step-by-Step Preparation Guide by EduPristine Hey there future US CMAs! If you're thinking about Read More

2023-09-27

Key Reasons Why Upskilling is Important

As we navigate the challenging yet exciting journey of studying finance and accounting, we wanted to share some valuable advice Read More

2023-06-27

All About Evolving Aviation Industry

India’s aviation industry has witnessed significant transformations in recent years, with the emergence of low-cost carriers, the expansion of domestic Read More

2023-06-16

How India’s Digital Payment Revolution is Reshaping the Economy

Hey there! So good to have you back again. In this blog, we will discuss the recent developments, explore the significance, Read More

2023-06-14

Understand the catastrophic impact of a possible US Debt Default

Hello there! Welcome to our new blog. In this blog post, we will explore the potential catastrophic effects of a Read More

2023-06-06

RBI Bids Farewell to Rs. 2000 Notes

Hello there! Welcome to our new blog. In this blog, we will explore the recent decision by the Reserve Bank Read More

2023-04-25

Key Insights from the Economic Survey 2022-2023

Hello there, students! How have you been? Today, we will explore more about the recent economic survey, 2022-2023. Economics Read More

2023-04-25

What is Digital Marketing? What is the objective?

Hey there! Ever wondered what is the main objective behind practicing digital marketing techniques? Digital marketing has now become a Read More

2023-04-25

Why you must consider being a Certified Management Accountant

Hey there! So good to have you back again. Are you someone who loves planning, analyzing, and adjusting monthly Read More

2023-02-24

Key Insights from the Economic Survey 2022-2023

Hello there, students! How have you been? Today, we will explore more about the recent economic survey, 2022-2023. Economics plays Read More

2023-02-14

What is Digital Marketing? What is the objective?

Hey there! Ever wondered what is the main objective behind practicing digital marketing techniques? Digital marketing has now become a Read More

2023-01-30

Why you must consider being a Certified Management Accountant

Hey there! So good to have you back again. Are you someone who loves planning, analyzing, and adjusting monthly budgets? Read More

2023-01-28

All About Classroom Training vs Online Training

Hello there, students! How have you been? Today, we will explore more about the recent economic survey, 2022-2023. Economics plays Read More

2023-01-03

All About Axis-Citi Acquisition

A significant move initiated by Axis Bank, India’s third largest private sector lender, to acquire Citibank’s retail business has become Read More

2022-12-28

Can vernacular edtech ever become mainstream?

Hey there! Glad to have you back again. Did you know that with the next half billion students coming from Read More

2022-12-26

Indian start-ups need to start taking corporate governance seriously, why?

Hey there! Glad to have you back again. Wondering why Indian start-ups require corporate governance? If yes, then this blog Read More

2022-11-22

How to Level up the Overall Digital Marketing Strategy?

Hello there! So good to have you back. Did you know that more than half of the brands today either Read More

2022-11-19

Snapchat for Business

Hey there! Welcome back again. In this blog, we will understand how to use Snapchat for businesses to stand out Read More

2022-11-18

What will Digital Marketing Look like in the Next 20 years?

Hey there! Do you wonder what digital marketing will look like in the next 20 years? If yes, then this Read More

2022-11-17

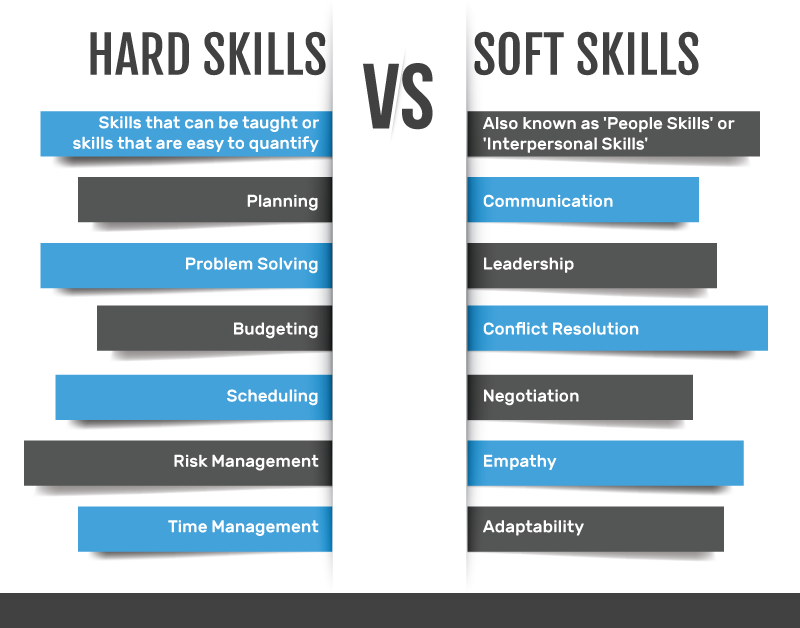

Importance of Soft Skills

Hey there! So good to have you back again. In this blog, we will understand the top 5 skills and Read More

2022-11-15

Why are Mr. Men and Little Miss characters all over the social media?

Hey there! Welcome back again. If you’re on social media, you must have probably come across Mr. Men and Little Read More

2022-11-14

How global firms are looking at the Indian investment market

Hey there! So good to have you back again. Wondering, how the global firms are looking at the Indian investment Read More

2022-09-14

Role of Keywords in Digital Marketing

Hey there! Welcome back again. Did you know that a proper keyword search lies at the heart of a successful Read More

2022-09-13

All About the Social Media Careers and the Skills to be Mastered

Hey there! Happy to have you back again. Did you know that social media careers are taking off? Well, social Read More

2022-09-12

All About Leadership in a Multicultural World

Hey there! Welcome back again. Ever wondered what a global mindset is? If yes, then this blog is a must-read Read More

2022-08-30

All about Metaverse and why is metaverse important for brands?

Hey there! Welcome back again. Wondering what exactly Metaverse is? Is it a video game? Or is it just another Read More

2022-08-26

Why will the Netflix business model need more than just a quick fix?

Hey there! So good to have you back again! Wondering why the Netflix model will take more than just a Read More

2022-07-25

Financial Models and How to Create them Effectively

Hey there! So good to have you back again. In this blog, we will understand how Finance Professionals can create Read More

2022-07-22

Top 5 Digital Marketing Trends to be Followed

Hey there! So good to have you back again. Wondering what marketers have been doing so far in 2022? If Read More

2022-07-19

Best Practices for Financial Management

Hey there! So good to have you back again. In this blog, we will discuss a few essential tips for Read More

2022-07-13

How did the crisis in Sri Lanka impact India?

Hey there! Welcome back again. In this blog, we will discuss how the crisis in Sri Lanka is impacting India. Read More

2022-06-27

Objectives of Risk Management

Hey there! So good to have you back again. In this blog, we will answer the most frequently asked question, Read More

2022-05-10

Career Options After Qualifying for the US CMA Course

Hey there! So good to have you back again. Are you curious and want to learn more about the job Read More

2022-05-07

Skills That Make You Proficient in Digital Marketing

Did you know that digital marketing is a dream job for many people today? Let us find out why? If you are Read More

2022-05-05

What Are The Different Types of Financial Markets?

Hey there! Welcome back once again. In the last few blogs, we discussed the financial markets and their functions. We Read More

2022-05-03

How Indian Students Can Pursue the US CPA?

Hey there! So good to have you back again! Are you also wondering how can Indian students acquire the international Read More

2022-05-02

Equity Derivatives and Benefits of Equity Derivatives

Hey there! Welcome back again. Ever wondered what are Equity Derivatives? If yes, then this blog is a must-read. Equity Read More

2022-04-29

What are Black Swans in Risk Management?

Hey there! So good to have you back again. Are you wondering what the term “Black Swans” in risk management Read More

2022-04-28

Will Digital Marketing Replace Traditional Marketing?

Hey there! Welcome back again. One of the most frequently asked questions we often get is, will digital marketing ever Read More

2022-04-27

Functions of Financial Markets?

Hey there! Welcome back to another blog on finance. In the previous blog, we discussed what are financial markets and Read More

2022-04-26

How to Calculate GST (Goods and Services Tax)?

Hey there! So good to have you back again. Are you also keen on learning how to calculate GST? If Read More

2022-04-25

Why are Financial Markets Regulated?

Hey there! Welcome back again. Are you also curious and wondering why are financial markets regulated and why are they Read More

2022-04-22

Does an Accountant Need an MBA?

Hey there! Welcome back again. Are you the one among others who is confused and want to know whether an Read More

2022-04-21

Why is ACCA Not Recognized in The USA?

Hey there! Welcome back again. Have you ever wondered why is the ACCA course not recognized in the USA, but US CPA Read More

2022-04-20

Is the US CMA Course Appropriate for Working Professionals?

Hey there! Are you a working professional and want to pursue the US CMA course simultaneously while working full time? If yes, Read More

2022-04-19

What is a Derivative?

Derivatives are financial contracts that derive their value from the performance of an underlying asset, or group of assets, or Read More

2022-04-18

What is Derivative Market?

Did you know that derivatives are also considered advanced investing? Well, derivatives can be called secondary securities whose value is Read More

2022-04-16

Types of Acquisitions

Hey there! Welcome back once again. Have you ever wondered why do many acquisitions succeed just as many who fail? Read More

2022-04-15

Types of Mergers

Hey there! Welcome back again. In the previous blog, we discussed what are mergers and acquisitions. In this blog, we Read More

2022-04-14

What are Mergers and Acquisition?

Hey there! Welcome back again. Mergers and Acquisition sound quite familiar right? But ever wondered why are Mergers and Acquisitions Read More

2022-04-12

Do Indian Companies Hire CFA’s?

Hey there! So good to have you back again. Are you planning to do CFA and wondering whether Indian companies Read More

2022-04-11

What Should I Study, US CMA or Digital Marketing?

Hey there! Welcome back again. Are you confused and wondering which course to study, US CMA or Digital Marketing? Well, Read More

2022-04-08

Types or Methods of Business Valuation

Hey there, Welcome back again. Let us understand what business valuation is and its different methods. Let us get started. Read More

2022-04-07

What is GST? What Are The Career Opportunities in GST (Tax domain)?

The tax system in India has undergone tremendous changes since the introduction of GST. GST stands for Goods and Services Read More

2022-02-16

How to Manage Risks in a Business?

Hey there! Welcome back again. Do you know one of the most critical factors to be kept in mind while Read More

2022-02-15

How to Work On a Digital Marketing Project for Practice?

Hey there! Welcome back to another blog. We will be discussing the tips on how to work on a digital Read More

2022-02-13

What is Digital Marketing? What is the objective?

Hey there! Ever wondered what is the main objective behind practicing digital marketing techniques? Digital marketing has now become a Read More

2022-02-12

Is CA the only optimal career option for commerce graduates?

Are you also thinking about what is next after B.Com? Is pursuing CA the only option for commerce graduates? Let Read More

2022-02-11

All about the US CPA course

Topic: Is CPA preferable after CA? Are you a qualified Chartered Accountant and wondering what is next after CA? If Read More

2022-02-10

In your opinion, what makes a good Financial Model?

Are you aware that a good financial model can help multiple start-ups and small businesses? With this, now let us Read More

2022-02-09

What is Business Valuation?

Business valuation is the general process or result of determining the economic value of a company or a whole business or Read More

2022-02-08

Does CFA has any scope in India?

Is it worth becoming a CFA (Chartered Financial Analyst)? Is it worth investing nearly three years, spending about 900 study hours, and Read More

2022-02-07

Career Advice: Is doing the ACCA over a CA a better option?

Hey there! So good to have you back again. This blog is mainly for those who are confused regarding which Read More

2022-02-04

Which is a Better Career Option, CFA or FRM?

Hey there! Welcome to another blog where we discuss which course is better, the CFA course or the FRM course? We will be Read More

2022-02-02

What is the procedure for enrolment for the CPA program for beginners?

Hey there! So good to have you back again. Well, if you are planning to pursue the CPA course then Read More

2022-02-01

How Do People Judge the Quality of Financial Modeling?

Hey there! Welcome back again. Are you also wondering what is Financial Modeling, that everyone in the finance industry keeps talking Read More

2022-01-17

What is the Reality of a Career in Digital Marketing?

Hey there! Welcome back again. Do you wish to get better clarity on what is the actual reality of a Read More

2022-01-14

Which is Better CMA or CIMA?

CMA and CIMA sound quite similar right? Are they the same? Are you also confused and wondering which one is Read More

2022-01-13

Is CFA in India Good for a Career?

Hey there! Welcome back again. Are you thinking about how good is the CFA as a career option in India? Let’s deep Read More

2022-01-12

I Desire to Get an ACCA Degree, but the Tuition is too Expensive. Why is the ACCA Course Expensive?

Hey there! So good to have you back again. Today, we will be answering the most frequent question which is, Read More

2022-01-11

Are There Any Job-Oriented Courses After Completing Graduation?

Hey there! Congratulations on completing your graduation. Are you now ready and excited to pursue job-oriented courses that will help you secure Read More

2022-01-10

Is Financial Modeling from EduPristine Worth It?

Hey there! Welcome back again. Let me begin by asking you a very simple question which is, did you know Read More

2022-01-07

Does Digital Marketing Have a Great Future Ahead?

Why Digital Marketing course is trending and has so much demand? What topics are covered under the Digital Marketing course syllabus? Is Digital Marketing Read More

2022-01-06

What are the Benefits of Pursuing FRM Course(GARP)?

You must have heard about the term FRM or Financial Risk Manager several times, but ever wondered what exactly is FRM, how Read More

2022-01-05

What is the Syllabus for CPA Course? Is it the Same as CA or Different?

Hello there! Welcome back again. Are your curious minds also wondering whether the syllabus for the US CPA course is similar to Read More

2022-01-04

What are The Top Skills a Commerce Student Must Have?

Hey there! So good to have you back again. Did you know companies are more inclined towards selecting candidates who Read More

2022-01-03

What are the Benefits of Learning Financial Modeling?

Do you ever wonder what does a Financial Modeler do? Some of you might also want to become a successful Read More

2021-10-21

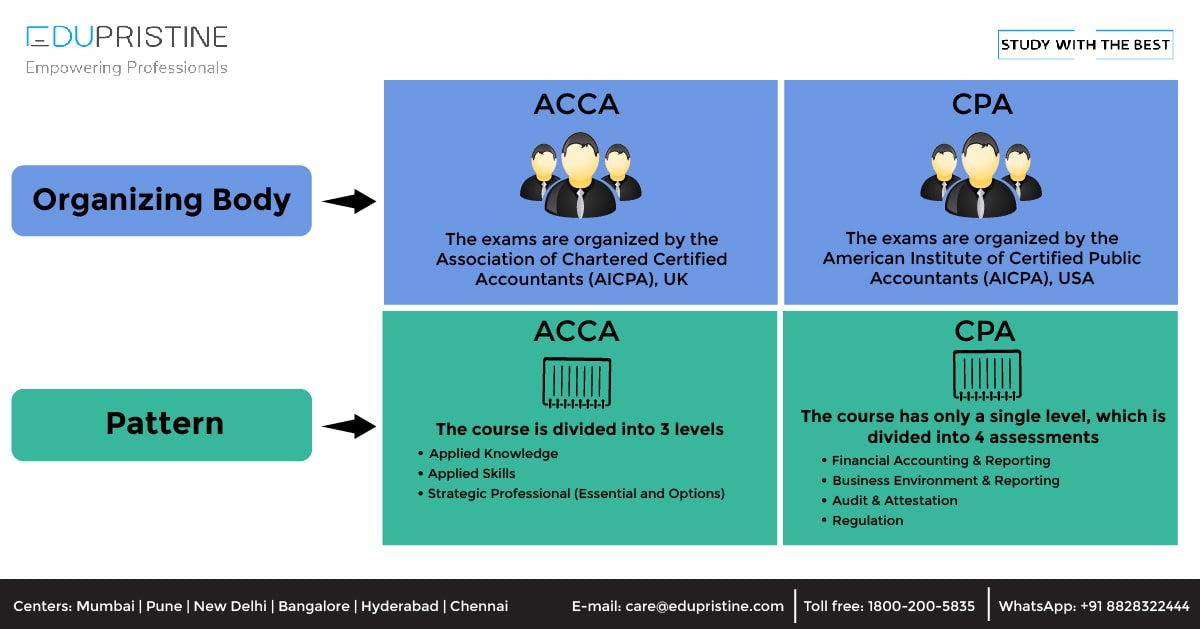

What is the difference between ACCA and CPA?

Accounting is a field that has endless job opportunities. It is the backbone of an organization. Be it any industry, Read More

2021-09-21

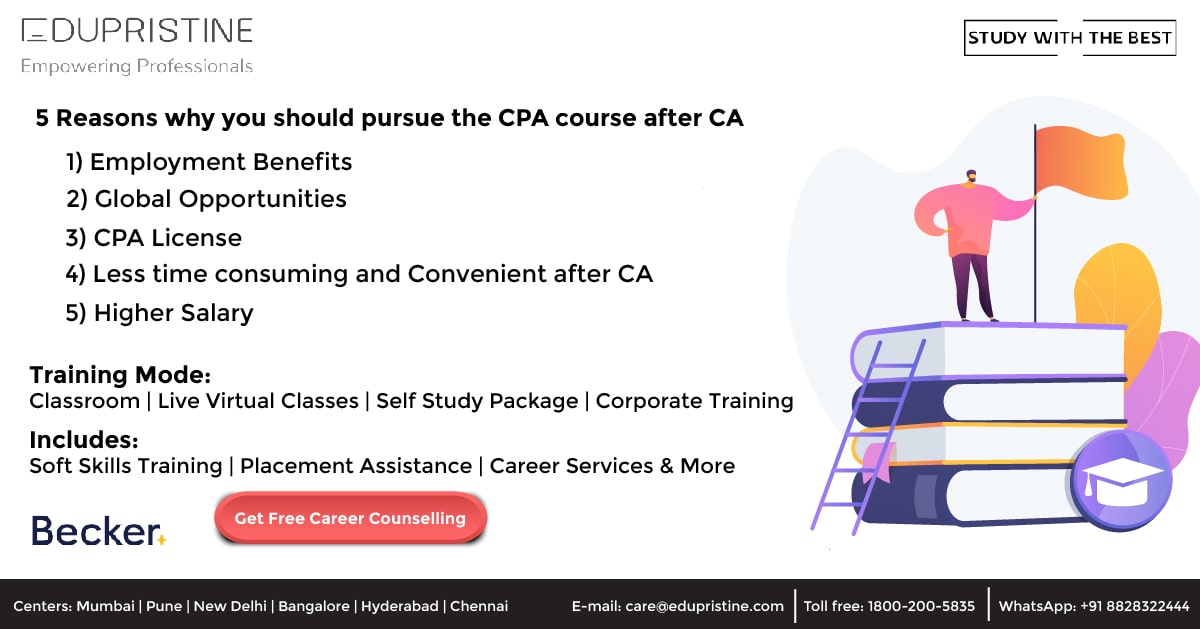

5 Reasons why you should pursue the CPA course after CA

CPA course, also known as Certified Public Accountant (CPA), is a globally recognized designation and is the highest standard of Read More

2020-10-21

How Opting for Full-Time Level I CFA Course Gives You an Edge Over Others

Chartered Financial Analyst (CFA course) is one of the most in-demand certifications in the field of finance and provides lucrative Read More

2020-08-22

A Complete Guide on ACCA Course Eligibility, Duration, Registration, Fees, Etc.

Why the ACCA course? ACCA is a global professional accounting body offering the Chartered Certified Accountant qualification (ACCA) and is Read More

2020-08-17

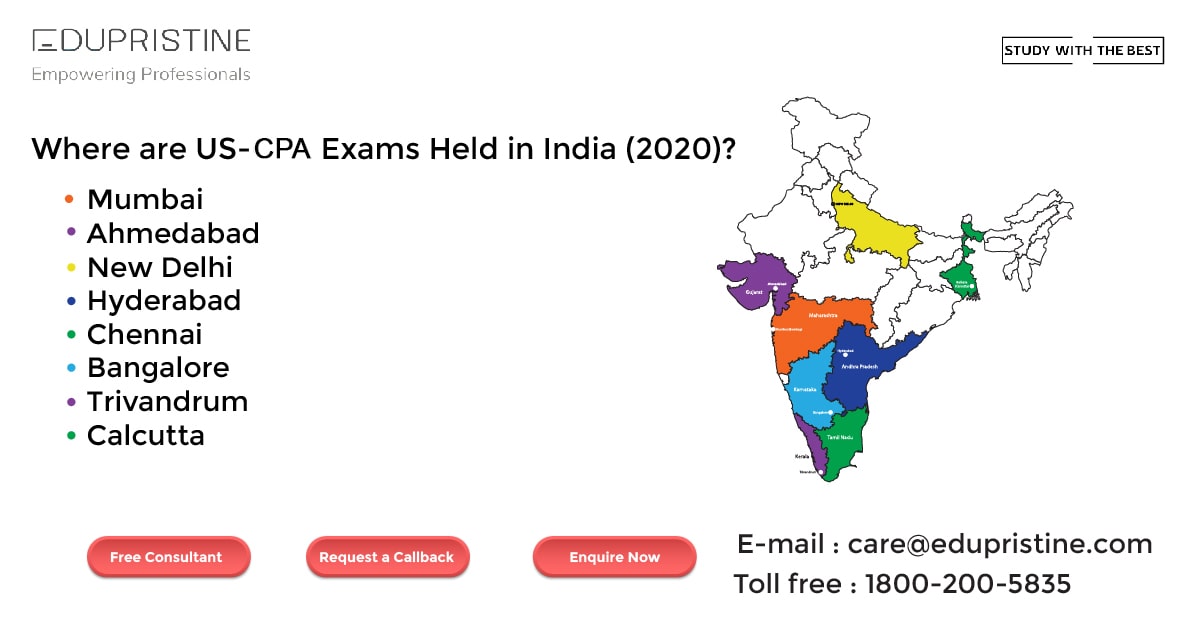

CPA Exam Registrations and Scheduling in India

CPA Exam Registration CPA stands for Certified Public Accountant and is one of the major certification courses in the field Read More

2020-05-18

What is Soft Skill Training ?

What is Soft Skill Training With the evolution of the business and client servicing industry, soft skills have started gaining Read More

2019-10-03

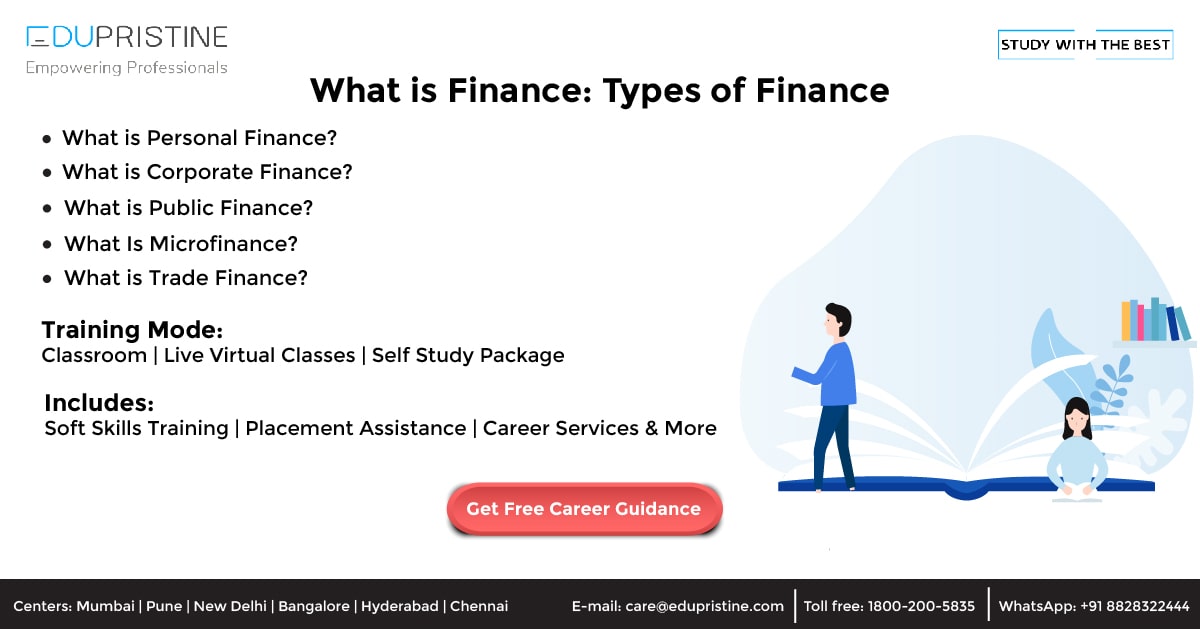

What is Finance: Types of Finance and Financial Instruments?

Finance is a major and vast topic to cover. Accounting and Finance are often used together, and some even deem Read More

2019-09-10

All you want to know about Chartered Accountant (CA)

Here's what you need to get started with the Chartered Accountant (CA) course Chartered Accountant is an honorable designation that Read More

2019-07-03

Soft Skills For The Hard World

Soft Skills Training - Reality Check: Whether we'™re talking in a team meeting or presenting in front of an audience, Read More

2019-05-26

What is the Importance Of Relative Valuation

Relative Valuation Generally speaking, ‘valuation’ can be defined as the process for finding the ‘value’ of anything. In the world Read More

2019-05-19

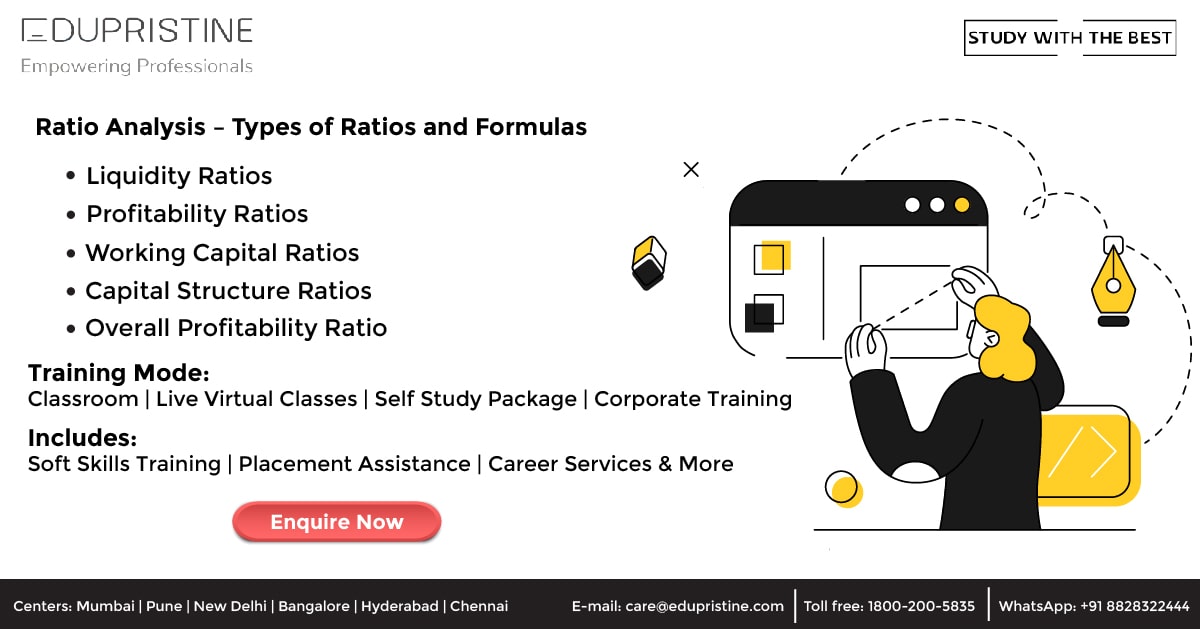

Ratio Analysis – Ratios Formulae

Ratio analysis'”the foundation of fundamental analysis'”helps to gain a deeper insight into the financial health and the current and probable Read More

2019-04-20

Excel Tricks: Text Functions in Excel

How to use Text Functions in Excel Excel is mostly about the numerical data, but at times you can Read More

2019-04-10

Explore the Top 12 Opportunities Which Will Take Your Career to the Next Levet [2020 – 2021]]

While writing the last paper of your final B.Com exam, a plethora of thoughts go through your mind. A lot Read More

2018-10-28

Top 10 Accounting Firms

Over the years, the way of doing business has changed significantly. There are a number of factors which have contributed Read More

2018-10-10

Everything you want to know about the CMA certification

CMA Full Form: Certified Management Accountant (CMA) Going for the CMA certification is a great career move, especially when you Read More

2018-08-06

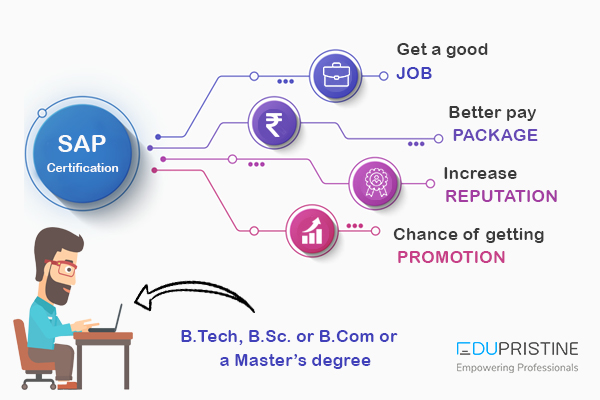

SAP certification – examination, eligibility and benefits

SAP certification help validate the expertise and experience of SAP partners, software users, customers and professionals who are looking to Read More

2018-08-03

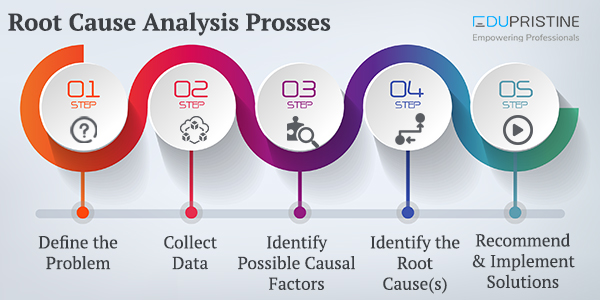

Root Cause Analysis

As the name suggests, Root Cause Analysis deals with identifying the origin of a problem and finding a solution for Read More

2018-06-26

Principles and Fundamental Concepts of Basic accounting

Accounting is extremely popular as the language of business language. Through this language, it is easy to analyze the financial Read More

2018-06-04

Know how to understand and interpret cash flow statement

A cash flow statement is essential to any business as it can be the basis of budgeting by assessing the Read More

2018-03-29

All you want to know about Sensitivity Analysis

What is Sensitivity Analysis? The technique used to determine how independent variable values will impact a particular dependent variable under Read More

2018-03-24

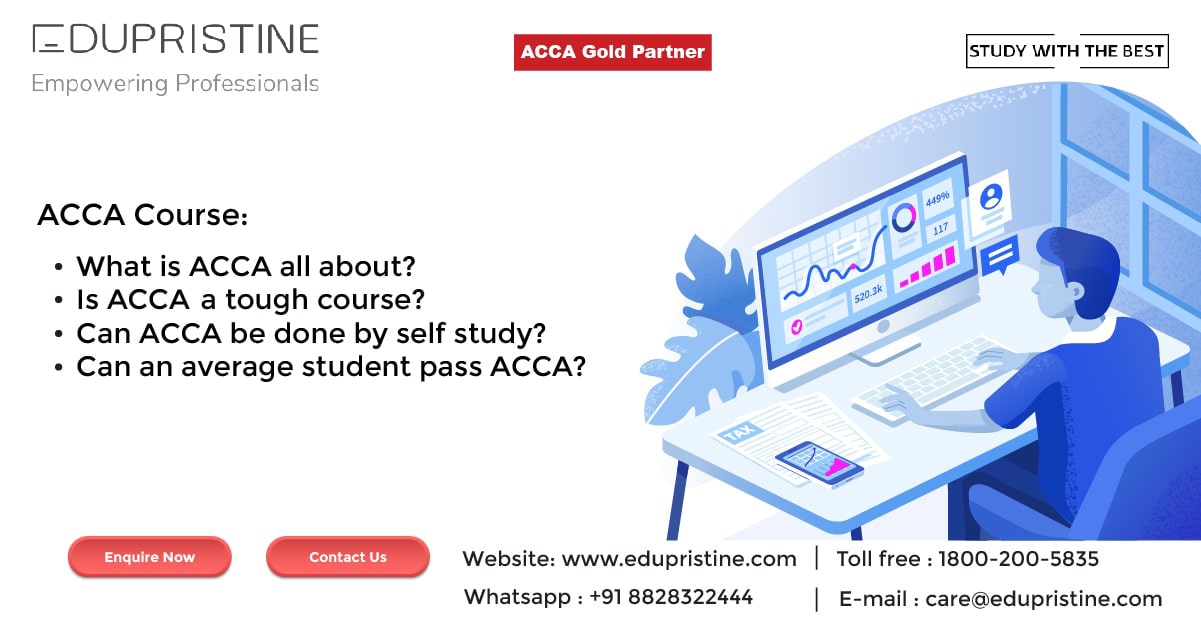

ACCA Full Form

ACCA - Association of Chartered Certified Accountants The role of strategic academic guidance in the life of a student is Read More

2018-02-25

Finding and Removing Duplicates in Excel

Did you ever come across a situation wherein, you see a lot of copied data or duplicates in excel and Read More

2018-02-07

Capital Budgeting: Techniques & Importance

In our last article, we talked about the Basics of Capital Budgeting, which covered the meaning, features and Capital Budgeting Read More

2018-01-14

Importance of Business Accounting for enterprises

Introduction: Importance of Accounting to your business The term Accounting is a very common one and we hear about the Read More

2018-01-11

Amalgamation Explained in detail

What is Amalgamation? Amalgamation is defined as the combination of one or more companies into a new entity. It includes: Read More

2018-01-08

Working Capital Management

What is Working Capital Management? Traditionally, investors, creditors and bankers have considered working capital as a critical element to watch, Read More

2017-12-30

Statistical Functions in Excel

People usually have love-hate relationship with statistics. When you get your formulas right you are in love with it and Read More

2017-12-07

Venture Capital

What is Venture Capital? It is a private or institutional investment made into early-stage / start-up companies (new ventures). As Read More

2017-12-02

Financial Reporting

In any industry, whether manufacturing or service, we have multiple departments, which function day in day out to achieve organizational Read More

2017-11-09

Cell References in Excel

While using excel, there may be times when you want to keep the values same while copying formulas. This can Read More

2017-09-24

Costing Methods & Important Cost Terms

Costs can be simply defined as the money or resources associated with a purchase / business transaction or any other Read More

2017-08-25

Balance sheet explained in detail

What is Balance Sheet? A balance sheet (also called the statement of financial position), can be defined as a statement Read More

2017-07-15

Cash Flow Statement

CASH IS KING;is a known fact, that it is the basis of any business. No bills, employees or for that Read More

2017-07-08

What are the career options after Mcom

Master of Commerce or M Com is a postgraduate Master Degree which specializes in commerce, accounting, management and economics related Read More

2017-06-07

What is Standard Deviation?

Standard Deviation Definition Standard Deviation is a statistical term used to measure the amount of variability or dispersion around an Read More

2017-04-21

Know how effective is CMA course compared to MBA in providing a dream job

There are various industries and sectors out there where you can grow and enhance your career. Management, Accounting, Finance, Engineering, Read More

2017-03-02

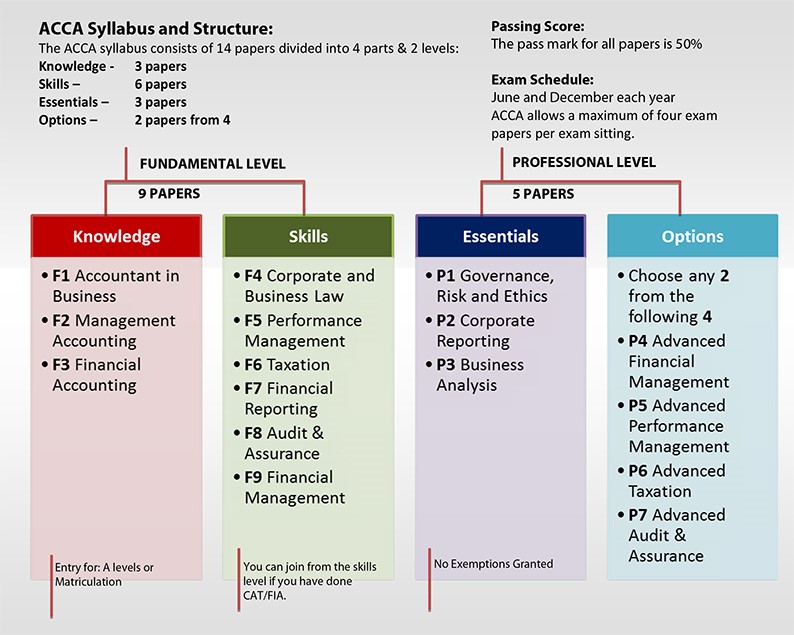

ACCA Exam Structure and Pattern

ACCA doesn't have a single definite pattern for all of its exams. Broadly the entire ACCA Exam Structure and Pattern Read More

2017-02-22

Comparison of CPA course with other courses

The Accounting industry offers you various opportunities to learn via various courses. You can choose which one suits your academic Read More

2017-02-08

Advantages and Application Process of FRM

FRM (Financial Risk Manager) Certification gives you a distinctive edge from the other risk management professionals operating in the Finance Read More

2017-01-03

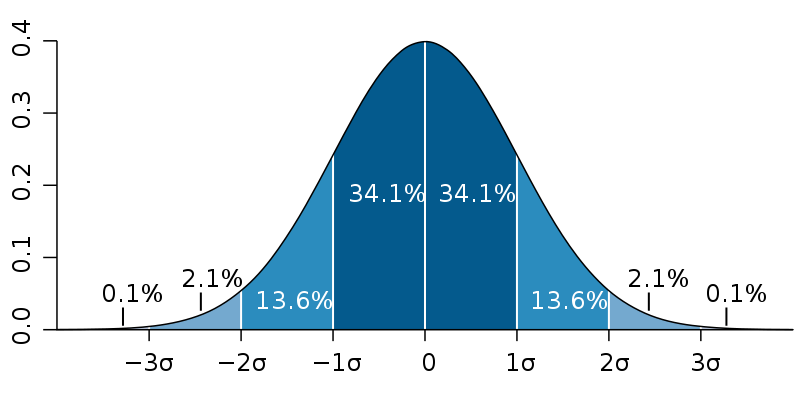

An insight into OTC Derivatives

What is Derivatives? Derivatives are defined as the type of security in which the price of the security depends/is derived Read More

2016-10-03

CPA Course Syllabus – Topics and Importance

A CPA requires a broad spectrum of knowledge and proficiency in it. The purpose of CPA exam syllabus is to Read More

2016-06-07

CFA® Study Planner

Most of the CFA® pursuers believe that CFA® Program tests are very difficult and arduous but that is not the Read More

2016-06-03

CPA Course details, application fees and benefits of doing it

A Certified Public Accountant (CPA) is the highest standard of competence in the field of Accountancy across the globe. The Read More

2016-05-31

All Important About CFA® LEVEL 1 Syllabus

CFA® charter is one of the most exalted credentials of those who work in the financial sector or who make Read More

2016-01-18

All about Portfolio Management

What is a Portfolio? A portfolio can be defined as different investments tools namely stocks, shares, mutual funds, bonds, cash Read More

2015-11-25

Cost Management: Meaning, Techniques & Advantages

What is Cost? Cost is defined as the monetary valuation of effort, material, resources, time consumed, risk and opportunity forgone Read More

2015-10-19

How to get into Big 4 Accounting Firms?

We all have some career objectives and aspirations. For higher studies like MBA, CA, CPA, ACCA, CFA etc. one has Read More

2015-10-13

FRM Question Bank

For every exam, time management is very important and everyone wants a precise course content in a prioritized manner along Read More

2015-09-29

Top 10 Companies that hire CFA® Charterholders

A lot of hardwork and investment is required to prefix the words CFA® Program before your name and time and Read More

2015-08-18

Income Statement in detail

WHAT IS INCOME STATEMENT? The income statement is one of the important primary financial statements provided by organizations. It presents Read More

2015-08-12

KPIs for Business Analysts

A business analyst's role in an IT project is to ensure that all requirements of the client are captured and Read More

2015-08-03

Annual Report

What is an Annual Report: The single source of getting information about any company whether it is the past or Read More

2015-07-01

Capital Budgeting

WHAT IS CAPITAL BUDGETING? Capital budgeting is a company’s formal process used for evaluating potential expenditures or investments that are Read More

2015-06-16

Mergers and Acquisitions

What is Mergers & Acquisitions? Mergers and acquisitions (M&A) are defined as consolidation of companies. Differentiating the two terms, Mergers Read More

2015-06-15

Detecting Multicollinearity

"In my previous blog “ How to deal with Multicollinearity ”, I theoretically discussed about definition of multicollinearity and what Read More

2015-05-26

Analysis of Financial Statement of a Company

One of the major aspects while taking a right investment decision is to analyze the financial statements of any company. Read More

2015-03-24

8 Excel functions that every Data Analyst must know

Are you a data analyst or looking for a career as a data analyst??? Well then, today's article is dedicated Read More

2015-03-24

Duckworth-Lewis Method

Duckworth-Lewis method(D/L method) is a mathematical function defined to set and calculate the target score for the team batting second Read More

2015-02-28

6 Most Common Excel Errors

Hashtags look cool when seen on Twitter or Facebook but as soon as they start appearing in Excel sheet, you Read More

2015-02-23

Rule Precedence in Conditional Formatting

Conditional Formatting in Excel makes the things easier and user friendly, but at times it may also make it quite Read More

2014-12-10

Types of Investment Banking jobs

Investment banking is one of the most attractive industry to work in. not only for people with formal education in Read More

2014-08-29

FRM Part 1 syllabus

Shut your doors, drop the drapes on your windows and don't bother looking at the clock because it's always the Read More

2014-08-20

Ratio Analysis – Introduction

Introduction The term 'ratio analysis'refers to the analysis of the financial statements in conjunction with the interpretations of financial results Read More

2014-08-20

Ratio Analysis – Classification of ratios and Liquidity Ratio

In our previous blog post we discussed ratio analysis. In this blog post we will explain classification of ratios and Read More

2014-05-23

Bootstrapping Solution

What is the Bootstrapping method? Bootstrapping is a method for constructing a zero-coupon yield curve from the prices of a Read More

2013-11-13

Dell’s Leveraged Buyout: A Real-life Case Study

Acquisitions Acquisitions or takeovers are a transaction or process wherein one company (commonly called as acquirer) or an investor acquires Read More

2013-08-08

Cash Flow Statement: Learn to create Cash Flow Statement Template in Excel

What is a Cash Flow Statement? In financial accounting, a Cash Flow Statement, also known as Statement of Cash Flow, Read More

2010-02-07